A Health Reimbursement Arrangement (HRA) is an employer-provided medical reimbursement plan. Employees are reimbursed tax-free for qualified medical expenses (for individuals, spouses and/or dependents) from this plan, which is funded solely by the employer.

How can an HRA help employers save money?

- Employers can choose to offer a health plan with a higher deductible at a lower monthly cost and utilize an HRA to help employees with out-of-pocket expenses. (These types of higher deductible health plans are not the same as Qualified High Deductible Health Plans (HDHPs), which are designed to be used with Health Savings Accounts (HSAs).)

- HRA funds are only used for medical care that employees actually receive, so employers may avoid paying for coverage their employees don’t use.

- Employers decide how much to contribute to their employees’ HRAs.

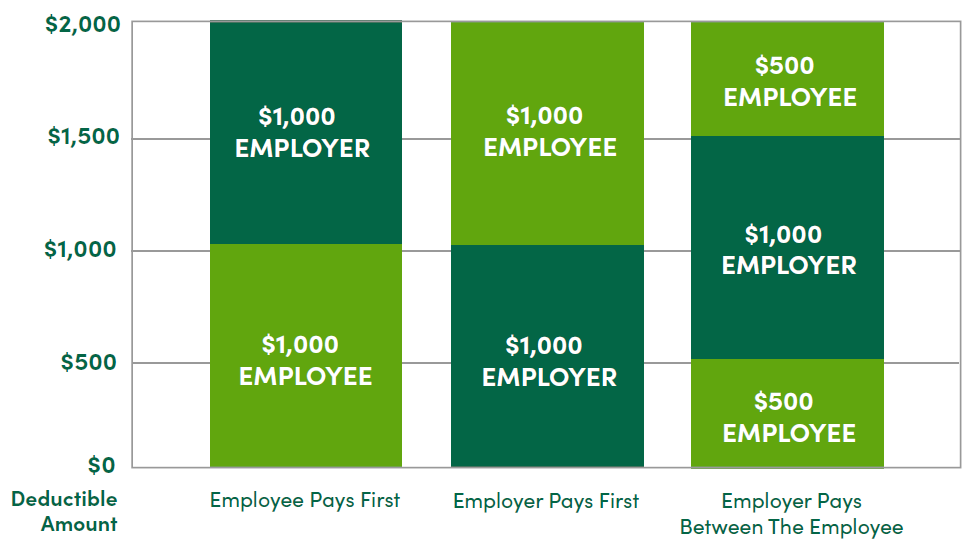

- Employers decide who pays for medical care first — the employer or the employee.

- Because employees are involved in paying for and getting reimbursed through an HRA, they may shop more carefully for medical care.

How does an HRA work for employees?

- Employees can be reimbursed tax-free for qualified out-of-pocket medical and dental expenses.

- Employees can use an HRA alongside the benefits of a comprehensive health plan.

Flexibility in Employer and Employee Cost Split

HRAs offer flexibility in how qualified medical expenses are split between the employer and employee. Here are three examples of cost splits for a health plan with a $2,000 deductible.

How do HRAs differ from HSAs?

Both HRAs and HSAs can help pay for qualified out-of-pocket medical expenses. Otherwise, the features of these plans differ substantially.

HRA Versus HSA Comparison

Health Reimbursement Arrangements

Employer owned

Specific to employer

Funded as needed

Funded by employer only

Rollover optional

Remains an employer asset

Health Savings Accounts

Individually owned

Portable

Funded before use

Contributions made by employee, employer, or others on owner’s behalf

Balance rolls over at year-end

Can be used as a savings/investment vehicle for future medical expenses

Must be used with a qualified HDHP

Learn more about the differences between Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs).

How Employers Can Set Up an HRA

When you’re ready to set up an HRA, consider the following steps:

- Decide how much to contribute annually.

- Determine when the plan will begin.

- Develop plan documents.

- Educate employees about how the plan works.

- Seek help from a licensed tax professional, attorney or benefits specialist to help ensure compliance.

Help Your Employees Start Well. Stay Well. Finish Well®.

At GuideStone®, we come alongside you with biblically based health plans to help your pastors and church staff lead resilient lives as they advance the Kingdom of God. For more information, contact us at Insurance@GuideStone.org or 1-844-INS-GUIDE (1-844-467-4843), Monday through Friday, from 7 a.m. to 6 p.m. CT.

GuideStone welcomes the opportunity to share this general information. However, this information is not intended to be relied upon as legal advice.