There’s no one-size-fits-all health plan for everyone. That’s why we’ve developed six steps to choosing a health plan that balances affordability with your health needs and life stage.

As you consider your plan options, weigh the following factors:

Look at last year’s health care expenses, including:

Then, consider any changes that you foresee in the following year. Do you plan to start a family? Will you soon be an empty nester? Do you anticipate needing a costly medical procedure? Will you begin a maintenance medication?

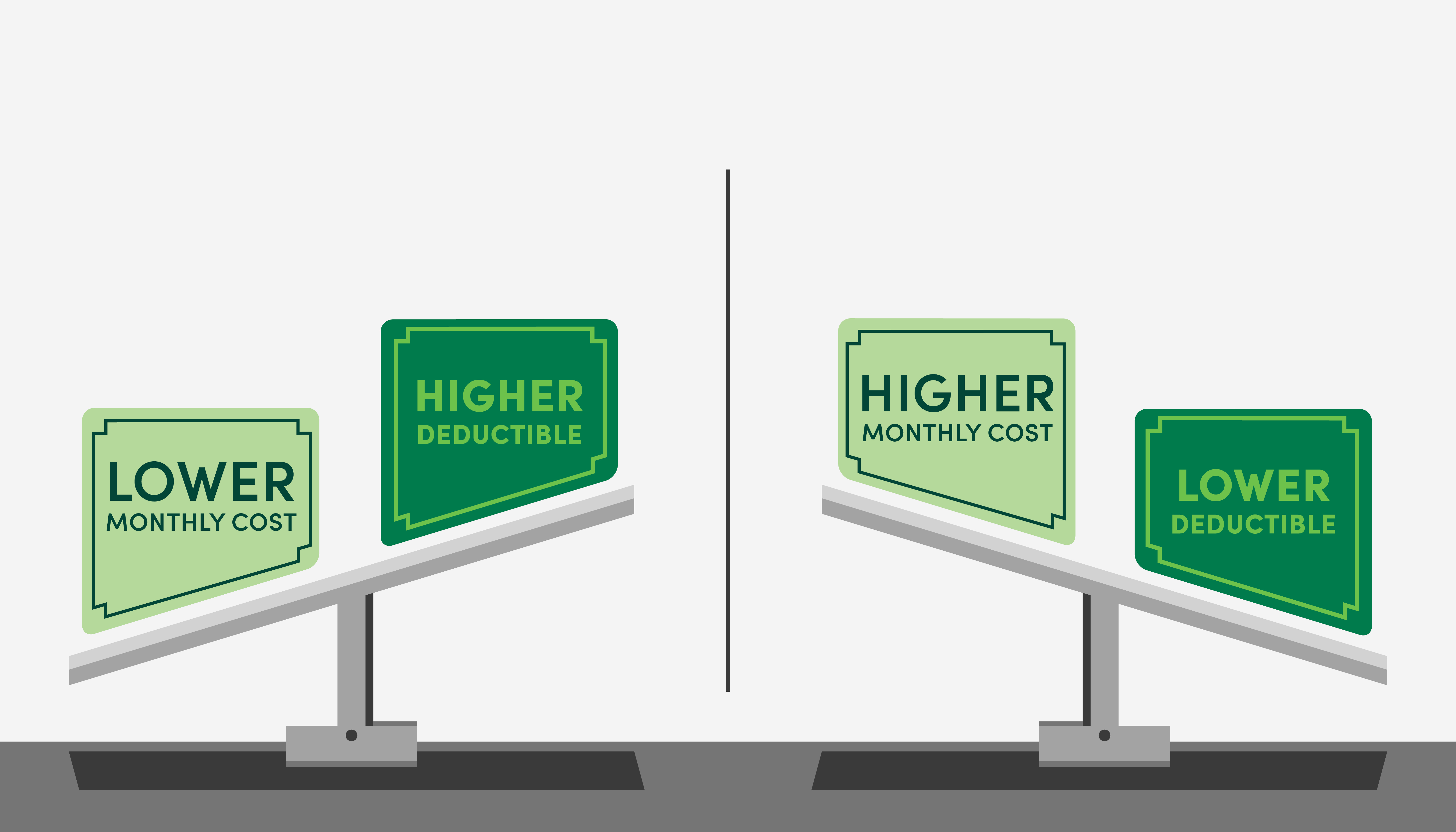

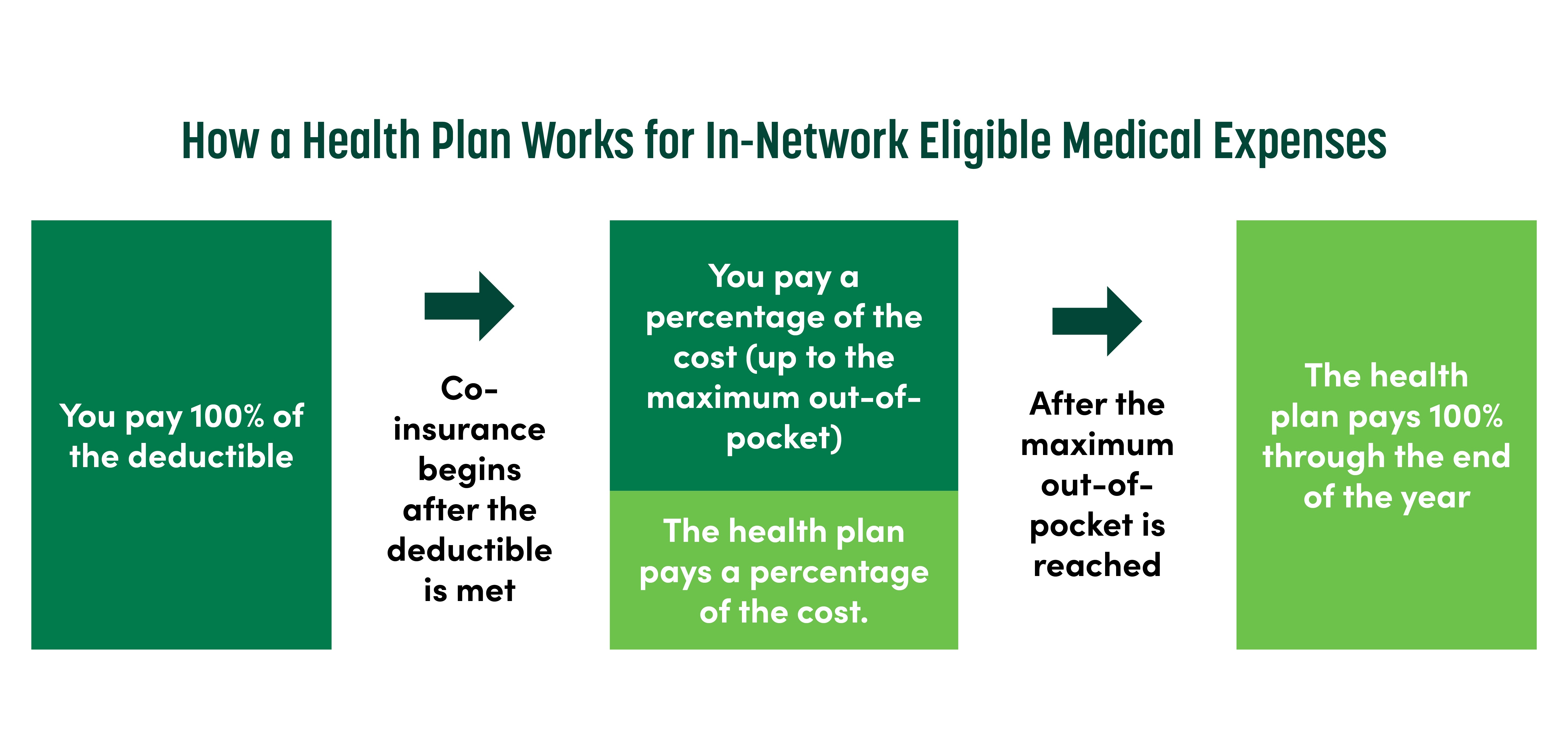

The deductible is the amount you pay out-of-pocket before your plan’s co-insurance kicks in. The lower the deductible, the more the health plan typically costs.

If you rarely meet your health plan’s deductible, consider selecting a higher-deductible plan. The monthly cost will be lower, and you won’t pay for coverage you may not need.

To determine the deductible that best fits your needs, ask yourself:

The co-insurance is the amount your plan pays for eligible services after you meet your deductible.

For example, a plan may have 80%/20% co-insurance. This means that after your deductible is met, the plan will pay 80%, and you’ll pay 20% of future costs. (Plans have a maximum out-of-pocket amount that limits how much you can spend on in-network eligible medical expenses in a year.)

If you don’t usually meet your annual deductible, the co-insurance is a less critical factor. If you do usually meet your yearly deductible, consider your estimated portion of the co-insurance.

To determine a plan’s annual cost, multiply the monthly rate by 12. But remember, this is the cost of having the plan, not using it. You’ll pay this fixed amount each month regardless of whether you’ve used health care services.

Now, determine the total cost to have the plan and use it.

Deductible + Co-insurance + Annual Cost of Coverage = Total Cost

Once you’ve selected and enrolled in a health plan, explore ways to minimize costs:

Choosing a health plan can be challenging, so we’re here to help. If you’re considering a GuideStone health plan, call us to walk through your options together. For more information, contact us at Insurance@GuideStone.org or 1-844-INS-GUIDE (1-844-467-4843), Monday through Friday, from 7 a.m. to 6 p.m. CT.

GuideStone welcomes the opportunity to share this general information. However, this article is not intended to be relied upon as legal advice, tax advice, or medical advice, diagnosis or treatment.